عرض العناصر حسب علامة : الذكاء الاصطناعي

الإثنين, 03 أكتوبر 2022 12:53

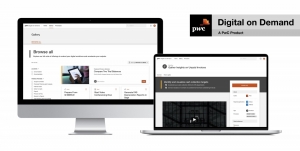

برايس ووترهاوس كوبرز تطرح تطبيقات الذكاء الاصطناعي الضريبية والمحاسبية

تطرح برايس ووترهاوس كوبرز تطبيقات الذكاء الاصطناعي الضريبية والمحاسبية

معلومات إضافية

-

المحتوى بالإنجليزية

PwC rolls out tax and accounting AI apps

By Michael Cohn

February 24, 2021, 5:40 p.m. EST

3 Min Read

Facebook

Twitter

LinkedIn

Email

Show more sharing options

PricewaterhouseCoopers is turning some of the digital tools it developed internally to train its staff into artificial intelligence products its clients can use in their finance departments.

The Big Four firm has packaged together the products it’s developed over the past three and a half years into a set of applications it calls Digital on Demand. They include apps for analyzing invoices for fraud, identifying cost reductions from credit card bills, and automatically reading and processing details from tax forms, invoices and other financial documents.

The online tools build on the ProEdge upskilling apps the firm showcased last fall for training employees (see story). That started with its own employees, but now PwC is rolling them out to clients, many of whom are working remotely during the pandemic.

Managing Your Firm in a Post-COVID World

Think beyond the pandemic with exclusive resources to help you build a thriving virtual practice.

SPONSORED BY INTUIT ACCOUNTANTS

“A couple of years ago, we started our digital journey at PwC, where we really said it’s not just about putting technology in our people’s hands, but we really have to digitally upskill our workforce,” said PwC Labs and tax technology leader Michael Shehab. “We’ve been on that journey for about three and a half to four years. As part of our digital upskilling journey, it was not our original intent, but we realized we had created a lot of intellectual property in technology. As we upskilled our employees, we realized the industry and communities needed a lot of upskilling as well.”

PwC tried to make the tools as usable and familiar as online shopping apps. The firm has now provided its clients with around 350 “digital accelerators” for various uses.

“Whether you’re in a controllership, internal audit, a tax function, a finance department, or a forecasting department, we believe we have created a digital accelerator that can drive additional productivity,” said Shehab. “In the process of driving productivity for our clients, you’re also learning the tool and learning the technology and you’re digitally upskilling.”

After testing out the digital accelerators internally until they’re mature, PwC markets them to its clients. “Within the tax space, we have many assets that extract information from tax forms,” said Robin Stein, director of PwC Labs. “PwC’s AI models are incorporated within Digital on Demand, so the user has the benefit of PwC’s investment in data scientists and annotating models, and extracting information from tax forms. There are a number of data workflows to think about on state and local tax calculations, and being able to calculate that on a state by state basis, where PwC has the domain knowledge and makes sure the business logic is up to date. The user would be able to come in and leverage that by just downloading the app and using it.”

The tools can help clients deal with state and local tax audits by extracting information from tax forms, legal documents and other sources. “You have the ability to really take the words and numbers off of a page, digitize them and analyze them,” said Shehab.

Clients can use the apps to assess the impact of recent tax and finance legislation like the CARES Act on their company. “There are a number of visualizations that will model out the impact of the changes in tax legislation,” said Stein. “That’s definitely of primary importance for clients right now.”

PwC clients are using the apps in various industries, including financial services and manufacturing, but tech clients have been using them the most. “The technology industry tends to be savvy, and they like modern-day tools like this, so we’ve had a lot of success with the technology industry,” said Shehab.

Corporate clients can use the tools for modeling the multinational provisions of the U.S. tax system. “At this point in time, we’re not focused on global taxes, but some of the international components that go into a U.S. tax return,” said Shehab.

So far, the Digital on Demand set of tools has attracted positive interest from clients since PwC made the apps available in December. “It’s been a pretty overwhelming response in the market in this post-COVID environment,” said Shehab. “We didn’t release it because of COVID, but everyone’s working virtually. Everyone’s concerned about how to continue to upskill their workers in this not-in-person environment, so this has hit very well. This really enables you to drive more productivity and in a very digital, virtual way.”

He sees Digital on Demand as a follow-up to the ProEdge digital training tools that PwC made available last fall and predicts that more of them will be coming in the future. “You’re going to see a pattern more and more from PwC that we’re taking all of our intellectual property and turning it into products and offerings to the market,” he said.

نشر في

تكنولوجيا المعلومات

الأربعاء, 21 سبتمبر 2022 13:07

نصائح واتجاهات التوظيف لعام 2021

من التوسع المفاجئ في العمل عن بُعد إلى طلبات خدمة العملاء الجديدة، كان لوباء COVID-19 آثار كبيرة على كيفية قيام شركات المحاسبة بأعمالها

معلومات إضافية

-

المحتوى بالإنجليزية

The Future of Finance: Hiring Tips And Trends For 2021

From the sudden expansion in remote working to new client service requests, the COVID-19 pandemic has had significant effects on how CPA firms do business. And while many disruptions might be behind us, the aftershocks will rumble on for some time.

Paul McDonald

Pandemic-driven changes creating benefits

As leaders scrambled to put new processes in place to navigate the effects of COVID-19 on the business, they have made progress in a number of areas. In a survey of senior managers:

41% say leadership communication is better now than it was pre-pandemic

37% think collaboration has improved

31% feel like there’s been substantial innovation over the past few months

Perhaps the most positive development is the way some companies have reimagined the hiring process. Of companies asked about their hiring methods in the age of social distancing:

57% are conducting interviews and onboarding remotely

40% have shortened the end-to-end hiring process

38% have advertised fully remote positions

These changes can help you act quickly and decisively when you’ve identified the right candidate for a position. And the prevalence of remote working means you can look further afield for skilled staff, giving your company access to a deeper pool of talent.

Accounting staff are in demand

One aspect hasn’t changed: It’s still a competitive hiring market for financial talent. You’ll have to fight hard for the best performers because many companies are ramping up recruitment. For example:

● Public accountants are a lifeline for small and midsize businesses right now. They’re helping clients navigate unpredictable cashflows, as well as shifting compliance requirements.

● Corporate accountants are tasked with finding new efficiencies that will keep businesses viable during financial turbulence.

● Government accounting departments have been forced to scale up quickly to address a raft of unprecedented financial aid packages.

● Financial services institutions are helping clients secure credit and reorganize liabilities during tough times.

● Healthcare companies need staff to deal with billing, reconciliations and new payment processes.

Retention still a concern

Skilled professionals are making career moves, even during a pandemic, and retention remains paramount. Unemployment is higher, but not that high for those with specialized skill sets, so in-demand accountants could be tempted to join another company. For businesses with currently lean staff levels, even the loss of a single skilled professional could be a serious blow.

In a separate Robert Half survey highlighted in the 2021 Salary Guide, more than eight in 10 managers said they are worried about losing valued employees. Here are their primary concerns:

· 55% are worried about losing staff over morale-related issues

· 50% have employees who are facing burnout from heavy workloads

· 37% imposed salary cuts with no prospect of raises in the immediate future

Salaries remain stable

Median salaries are fairly stable across the board, though (as ever) the best candidates in the hottest sectors will be looking to negotiate a bump in pay. Use the Robert Half salary calculator to ensure you’re paying at least market value for your region.

Remote work is the new normal

The pandemic sparked a mass exodus from corporate to home offices. This was jarring for many workers, but research in the guide suggests that few employees are in a hurry to get back to company HQ. Almost three in four workers say they want to keep working from home after the pandemic.

When hiring, you’ll need to balance the desire of highly skilled candidates to work from home with the needs of the organization. Fortunately, you’ll be in a much better position to make these calls than you were in late March, since your firm should now have more data and anecdotal evidence to draw on regarding the productivity and morale of remote workers across your teams.

Tech skills are essential …

If you’re looking to add to your remote teams, new recruits should be tech savvy and capable of learning new systems with little or no in-person training. They need to be able to work with cloud-based systems, understand IT security protocols and be comfortable using digital communication tools. Home-based workers also need to have the basic IT skills to solve common computer and networking issues, as they won’t have hands-on support from a helpdesk technician.

However, while it’s easy to be dazzled by the new and exciting world of remote working, keep in mind that collaborative platforms like Slack and Microsoft Teams are much easier to master than specialized accounting software. Microsoft Excel, QuickBooks (for smaller businesses), enterprise resource planning (ERP) systems and similar applications remain the gold standards, and you should assess candidates’ resumes accordingly.

… but so are soft skills

When is an Excel wizard with a fully equipped home office wrong for your organization? Perhaps when their track record or interview performance suggest that they struggle to collaborate with colleagues, or that they find it difficult to adapt to changing goals and circumstances. In these challenging times, soft skills such as critical thinking, resilience and flexibility can be every bit as important as technical expertise.

The need for these attributes is not driven just by the pandemic. As new technology such as AI becomes an integral part of finance jobs, you’ll place a greater emphasis on the kind of human values that can’t be replaced by an algorithm.

Flexible staffing is the future

Flexible staffing — an adjustable mix of full-time and interim professionals — is a strategy many companies have long been using to temporarily access specialized expertise and scale their teams as needed without overburdening full-time staff. It is tailor made for the current situation. Asked why they worked with interim professionals, more than a third of senior managers said it was to remain agile during the economic turmoil.

Predicting the future has never been harder. But if 2020 has taught us anything, it’s that uncertain times reward companies that are nimble and innovative.

نشر في

موضوعات متنوعة

الثلاثاء, 24 مايو 2022 07:19

إنفوجرافيك.. مستقبل التسويق المحاسبي هو الإستراتيجية

نشر في

إنفوجرافيك

موسومة تحت

الإثنين, 03 أكتوبر 2022 12:52

ماذا تتوقع من الذكاء الاصطناعي 2.0؟

الذكاء الاصطناعي في أيام مجده الآن، مع تطبيقاته الموعودة التي يتم تحقيقها في مجموعة من مجالات الخدمة للمحاسبين

معلومات إضافية

-

المحتوى بالإنجليزية

AI, applied: What to expect from AI 2.0

By Ranica Arrowsmith

Artificial intelligence is in its glory days now, with its promised applications being realized in a range of service areas for accountants. But AI is for more than just automating processes and creating efficiencies — now is the time for firms to be creative, thinking about new industry-specific applications and firm-specific pain points where AI can play a role.

Springboarded by the establishment of its AI lab in 2019, Top 100 Firm Armanino has been seriously investing in artificial intelligence with an eye on remaining ahead of the curve on efficiencies and client service.

In 2020, the COVID-19 pandemic accelerated the adoption and development of many different technology areas. AI was one of them. Tom Mescall, partner-in-charge of consulting at Armanino, shares his thoughts on what artificial intelligence will bring to the accounting profession in the near future.

Industry-specific applications

“As we continue to invest in artificial intelligence, it’s going to be by industry,” Mescall said. “As we’ve gotten deeper into industries like SaaS, digital media advertising, nonprofits, performing arts, social services, real estate, hospitality, real estate, construction, it’s clear that the use of robotic process automation, AI and data analytics becomes pretty industry-specific.”

Many accountants choose to serve very specific verticals, getting to know them well

The importance of bots

A bot is essentially an AI program written to perform certain tasks, which can be very tasks, and they can be applied/deployed in any area that can be automated.

“Bots have been the area where CFOs have specifically looked to find efficiencies out of things like the month-end close, approvals and expense reports,” Mescall said. “Anything that needs to be approved is great for a bot. You can get program rules, validations and checks just like a human would do.”

Bots have been around for years — but now their technology is more sophisticated and usable than ever.They provide an opportunity for firms to solve targeted problems and gain efficiencies without a necessarily high investment.

“In the past 10 months, the deployment of bots has really accelerated,” Mescall added. “In the past, we were demystifying AI — it was on people’s tongues, but they didn’t know how to use it

Now companies are saying. ‘I have to use it because I need to be efficient.’”

Read more of Mescall’s thoughts here.

نشر في

تكنولوجيا المعلومات

موسومة تحت

الأربعاء, 20 يناير 2021 13:03

فتح الصندوق الأسود للذكاء الاصطناعي

وصف في السبعينيات من القرن الماضي أستاذ الروبوتات في طوكيو ماساهيرو موري، كيف تبدو الآلات أكثر شبهاً بالإنسان

معلومات إضافية

-

المحتوى بالإنجليزية

AI, applied: Opening the black box

By Ranica Arrowsmith

There’s a phrase for the uneasiness many of us feel when confronted with humanlike machines — the Uncanny Valley. Coined in the 1970s by Tokyo robotics professor Masahiro Mori, the phrase describes how as machines appear more humanlike, they become more appealing to humans — but only up to a point. After that, as they appear more humanlike but not quite, they inspire revulsion in the observer.

In the accounting profession, there is a similar uneasiness when dealing with the idea of AI, though it has nothing to with how the software looks. The technology has the potential for high-level automation of processes, ultimately saving a lot of time for the accountant, but with its ability to perform tasks that are traditionally the purview of human beings, does this mean a diminished role for the accountant, or even the loss of jobs?

The good news is, the experts don’t think so.

Justin Adams, whose company Anduin has just launched an AI-enabled accounts receivable platform, insists there is an “art” to billing that must remain in the AR process for it to be meaningful and profitable — the deep knowledge of a client over time, for example, can affect a billing relationship. And Samantha Bowling of Garbelman Winslow CPAs isn’t interested in simply speeding up the audit with AI — she wants to provide an audit of such high quality that it’s unquestionable. These types of service goals can only be achieved by marrying AI with the human professional, with all the professional’s experience, skepticism and emotional intelligence.

Artificial intelligence can have an air of mystery about it, to say nothing of a hint of the unnatural, with something we value as inherently human — intelligence — being created and inserted into something inanimate — a machine.

It makes sense that we feel this way. The programming precursor to what we today call artificial intelligence was neural networks, code that was inspired by and modeled on actual human neural networks in the brain. Today, artificially intelligent programs have the ability to observe patterns and use those to “learn” behaviors and responses, making the technology smarter and more usable over time.

It’s worth bearing in mind the various ways in which AI is already here, working in the background of the accounting and enterprise platforms you know well, automating processes and making software more efficient. All the user sees are the benefits. But the market is now seeing true AI platforms that apply machine learning to entire processes end to end, such as AR/AP. And the common theme among all use cases for such AI-rich platforms is time — the time it takes to adopt the software and to validate it, to train it enough for a firm to realize its benefits. The machine has to learn. This takes an investment both of money and patience, but for the willing, it’s worth it.

Today, artificial intelligence is transforming processes across the accounting profession, for those are ready to invest in and adopt it. It’s not just being practically applied in audit, where AI is being used for data analysis and anomaly detection — we will look at examples of AI transforming AR/AP, as well as explore the implications of AI in sales tax automation.

Accounts: Receivable

Despite … everything about this year, venture capital funding continued on an upward trend in 2020, with the third fiscal quarter bringing in the second highest amount of VC funding per quarter on record. Artificial intelligence is high on the list of hot tech, which makes it no surprise that Anduin was able to obtain seed funding and launch its first AI-powered product suite all during the COVID-19 pandemic.

Anduin co-founders Justin Adams and Pat Morrell have built an AI-driven accounts receivable platform, Intelligence-Based Billing, for accounting firms. The platform launched in December, so it remains to be seen how successful adoption will be, but the pair of entrepreneurs have succeeded before in the AI space. Prior to founding Anduin, Adams and Morrell started, grew and sold a company that made an AI-driven product for the health care space, all within two years. That whirlwind experience propelled them into their current venture, and their success made them attractive prospects for investors.

“We had zero health care background when we started Digitize.AI,” Morrell said. “But we went to CFOs of health care companies and asked them where their biggest pain point was. When they said ‘prior authorizations,’ I had to look it up on Wikipedia — but I knew that a manual process is a manual process, and can be automated.”

Adams and Morrell weren’t quite as clueless entering the accounting space. Adams had spent years working at Big Four firm PwC, first in a consultative capacity and then internally managing technology projects. When they asked accountants what they would change if they could wave a magic wand, accounts receivable was a common answer. The process, managed manually, is scattered and unwieldy, and even streamlined client portals don’t optimize the process for each individual client and their payment habits.

There’s an art to billing, Adams said, and the platform tries to preserve that for the accountant. “Think of it from a client’s perspective,” he said. “There’s tons of friction. It can be confusing. You could have received a service three months earlier, and when you get the invoice, you’re trying to remember what you’re paying for again.”

Intelligence-Based Billing is made up of four modules (which can be bought separately), handling invoicing, collection, payments and internal analytics. The platform automates the invoicing process so bills are sent in a timely manner, but it also learns a client’s payment habits over time. How many emails or messages does it take before an invoice is opened and viewed? How many contacts does it take before a client pays the bill? Each client is different, and therein lies the art. If a client typically pays an invoice after two emails and a phone call, Intelligence-Based Billing will “remember” that over time, optimizing the process for each firm-client relationship.

More “art” that the AI tries to replicate: The analytics feature can be used in part to automate, so to speak, that gut feeling accountants also have to pay attention to when it comes to value-based billing. For instance, Morrell pointed out, a firm may have worked a certain number of hours on a project, but with their sense of the market over the years, they know that a client might expect a certain discount. Each client perceives different aspects of a service as more valuable, and also might need different billing structures to remain a client in the long term. Intelligence-Based Billing pulls and analyzes data from across firm systems to inform this type of decision-making.

“The fundamental pain is the anxiety that firms are leaving money on the table; and that firms don’t have real visibility into their cash flows,” Morrell said. “On the partner level, it’s all about liberating them to focus on complex, creative, value-generating service delivery.”

Intelligence-Based Billing is new on the market, and is signing up “trailblazer firms” now as its first customers. Time will tell how successful it will be, but no matter what, Anduin is part of a small group of innovators bringing fully formed, AI-enabled automation to firms of all sizes, for everyday firm functions, and will help set the stage for what’s to come.

Accounts: Payable

Youngseung Kuk manages business outsourcing services for Top 100 Firm Armanino in Boise, Idaho. This year, Kuk spearheaded the implementation of Vic.ai, a platform that automates the accounts payable process using AI. Using AI to tackle AP for clients was “low-hanging fruit,” Kuk said, as all companies, no matter what type, have bills to pay.

Armanino uses Bill.com firmwide for all AP, so the firm worked with Vic.ai to integrate the software to make the end-to-end AP process more streamlined.

Kuk and his team are validating Vic.ai as they use it, adding clients slowly, one at a time, to make sure they give the program enough time to learn its clients and become highly efficient at its predictions. This is a key part of understanding AI — it takes time.

Software that runs on AI doesn’t operate like the software we’ve become accustomed to. It doesn’t perform an exact set of functions as programmed, and only as programmed. Artificial intelligence learns as it goes, which means that by the end of a certain period of time, the software will operate very differently for each client, each firm, each project.

Kuk estimates it will take Vic.ai three years to predict client behavior and needs at a close-to-perfect rate. The wait is worth it for the sheer amount of time it can give back to an accountant once the AP process for a client is basically fully automated.

Armanino has one client, a law firm, that has highly repetitive bills that don’t have too many complicated dimensions (i.e., company name, address, and so on, are usually in the same spot on the invoices). Within a few months of use, Vic.ai can now predict any given AP workflow for that client with about 80 percent accuracy. If this is true for this client, Kuk said, that’s enough to know it’s possible for the others. Currently, Armanino has 46 clients on Vic.ai, and plans to keep validating the software so it can add more in time.

“The time spent validating is worth it, because by the end, as a firm, we’re going to be so much more scalable,” Kuk said. “Once you free up some capacity, even just from an AP standpoint we can do a number of different things for our clients that add more value, like confirming all vendors have W-9s, for example, or reaching out to vendors proactively if they haven’t accepted an ACH payment. These are just some basic examples, but I think we’re at the tip of the iceberg and nowhere near the full potential of AI.”

“Two years ago, we made an investment in artificial intelligence in a big way. It became part of firmwide strategy,” explained Tom Mescall, partner-in-charge of consulting at the firm. “Most CEOs, CFOs and business operators know the headline of AI, but they don’t know how to apply it in a business setting. We’ve done a lot of work around demystifying AI and bringing real-world examples to light for clients.”

A relevant audit

Firms have been using AI products for anomaly detection and analytics in audit for a few years now. Companies like MindBridge AI came on the scene and started to show the profession the real-world implications of being able to read every piece of data in minutes, as opposed to just sampling data. Samantha Bowling, a partner at Garbelman Winslow CPAs, saw the opportunity in MindBridge AI three years ago, and brought the technology to her firm.

In 2017, while Bowling served on the Governing Council for the American Institute of CPAs, she listened to president and CEO Barry Melancon describe how Big Four firm KPMG was investing millions of dollars into AI-driven audit technology.

“He was talking about how they were going to take over the world,” Bowling recalled. “As a small-firm audit partner, I was concerned, because if the big firms are doing something, sometimes it doesn’t become available to us for a while, or ever. I was actually concerned about eventually having to find a new revenue source.”

She called her existing audit software provider and asked explicitly if they had plans to embed AI into their platform. They didn’t. So Bowling did some online research and found MindBridge AI.

Bowling says that Garbelman Winslow is still in the adoption phase of MindBridge. As is true with the other technologies featured here, there is no substitute for time to allow an artificial intelligence platform to live up to its true potential. She started by engaging MindBridge for just one audit, and then grew usage from there. It helped when MindBridge integrated with QuickBooks, which made data transfers easier.

The biggest benefit of applying artificial intelligence to audit, for Bowling, is the risk analysis.

“Now that there is a direct link between QuickBooks Online and MindBridge, it automatically connects and does the risk analysis,” Bowling said. “I used to think MindBridge was an audit stamping tool that looked at transactions and identified anomalies, directing our attention and telling us where to look. But I realized it’s actually a great risk assessment tool in the very beginning of an audit.”

Bowling explained that while audits are based in risk assessment, a lot of the time, auditors have no idea where the risk is. “We only have our professional skepticism — there’s no one to tell us the risk is in revenue or payroll,” she said. “Now we have something that tells us where it is at the outset. Audit assertions are built into it.”

But there is friction in adoption. Not every client is easy to work with in MindBridge. There is still a lot of manual work to be done to transfer data that is not in the cloud, for instance, to MindBridge AI’s platform.

“Everyone just wants it to be an easy thing — to upload the general ledger and get going — but I think they’d be remiss not to do this with at least one client, or start with their cloud-based clients first before going to challenging clients,” Bowling said. “People are looking for faster, better ways, but I went into this not to do a faster audit but a relevant audit.”

Bowling received CPA.com’s Innovative Practitioner Award in 2018 for her work bringing AI to Garbelman Winslow CPAs. She won in part for the fact that it is small business and nonprofit clients to which she is bringing AI-enabled services, which also has the side benefit of Bowling being able to pass the cost of using MindBridge to her clients by folding it into the billing package. Nonprofit clients don’t mind paying top dollar for service that guarantees an accurate risk assessment.

“Nonprofit clients don’t care about us passing the fee onto them to minimize risk as much as we do, because nonprofit board members are just worried about someone doing something wrong with the money and it being in the newspaper,” Bowling said. “So they’re happy to have a very good audit done, and pay for it.”

Every transaction in the world

When thinking about the application for artificial intelligence in tax, often we think about tax preparation, since there is a lot of room to automate it. In fact, Samantha Bowling said that if she could apply AI to any other service area at her firm, it would be tax: “The current process, with a mix of paper documents and e-returns, is asinine,” she said. “I can’t wait till the whole process is 100 percent automated.”

AI-related innovation in tax prep is moving slowly, although the Internal Revenue Service has started to use the technology in different capacities to detect tax evasion and other types of noncompliance. But of course, there are other areas of tax that are ripe for disruption with AI, and sales tax automation is one.

One of the companies working in this area, Avalara, has made investments in AI in recent years, one of which was acquiring Indix in 2019. Indix was based on an idea that founder Sanjay Parthasarathy had for creating a comprehensive index of retail product information online using artificial intelligence to aggregate the data. (The aggregator was built in layers, with a Google web crawler grabbing information from all over the internet, and then various smart algorithms working together to curate and organize that data.)

Brands and retailers could buy access to this database of information on mostly retail, but also some business-to-business, products, to enrich their catalogs, benchmark against competitors, and so on. Basically, Indix was built as a neutral aggregator of e-commerce inventory.

And now, Avalara owns that AI-built index of more than 4 billion products. This means that Avalara can fold categorization data for much of the world’s online inventory of products in with its tax content database, which includes international product codes and classifications; taxability rules; exemption conditions; tax holidays; jurisdictions; boundaries; tax rates; thresholds and registration, compliance, and return preparation and filing requirements.

If this list sounds daunting, that’s kind of the point: Avalara’s mission is to “to be a part of every transaction in the world.” Without AI enabling at least some of this technology, this would be an impossible goal.

“When you buy a tax compliance product or suite, you want to be able to start using it tomorrow,” said Parthasarathy, who now serves as chief product officer for Avalara. “However, you know that before you can use an automated system, you have to make sure the tax nexus is right, the catalog is mapped to the tax code, a set of things that take time and research. If you want to start selling internationally, and you therefore need to start using harmonized tax codes — if it’s going to take nine months to do it, that’s lost value. We can get you going right away.”

Before Parthasarathy founded Indix, he spent almost two decades at Microsoft. He ended his career there in 2009 as corporate vice president of the Startup Business Accelerator program, a program he created; and he was director of Bill Gates’ 1997 trip to India, which led to a significant investment in that country by the software giant.

When talking about historical AI, Parthasarathy will sometimes use the term neural networks, which are indeed the statistical model programs ancestor to what we call AI today. His knowledge of AI is deep and historical, from having spent so many years helping build one of the most innovative companies in recent history. From his vantage point, he sees both the immense possibilities of AI, as well as the risks.

“There are risks in tax — compliance has potential penalties if done incorrectly,” he commented. “You’re doing it on behalf of somebody, so you want to make sure it is accurate and appropriate. You probably want actual people to keep an eye on it, rather than let AI run everything, even if one day it can. There is an ethical risk — when you have all this data, what is the responsibility of the government and companies to treat it as private data?”

نشر في

تكنولوجيا المعلومات

الأربعاء, 30 ديسمبر 2020 17:25

معهد المحاسبين الإداريين يشهد نموًا في عام 2020 على الرغم من الجائحة

معهد المحاسبين الإداريين يشهد نموًا في عام 2020 على الرغم من الاضطرابات الناجمة عن فيروس كورونا

نشر في

موضوعات متنوعة

الثلاثاء, 15 ديسمبر 2020 12:43

خطر تعطل المواهب يلوح في الأفق في عام 2021

نظرًا لأن المدققين الداخليين يضعون اللمسات الأخيرة على تقييماتهم للمخاطر قبل إعداد خطط تدقيقهم لعام 2021، فهناك خطر واحد لا ينبغي إغفاله

نشر في

موضوعات متنوعة

الخميس, 10 ديسمبر 2020 14:09

أربعة اتجاهات تقنية أساسية للإنتاجية في عام 2021

لا شك أن عام 2020 كان عامًا مجنونًا في جميع أنحاء العالم

نشر في

تكنولوجيا المعلومات

الأربعاء, 09 ديسمبر 2020 12:48

مستقبل التسويق المحاسبي هو الإستراتيجية

عندما ننظر إلى الوراء في عام 2020، ماذا سنتذكر؟ COVID-19 ، بالتأكيد

نشر في

موضوعات متنوعة

الإثنين, 07 ديسمبر 2020 14:08

مواجهة المحاسبين لتيار الأتمتة المتزايدة

يمكن للمحاسبين مواجهة تيار الأتمتة المتزايدة

نشر في

تكنولوجيا المعلومات

موسومة تحت