عرض العناصر حسب علامة : عقود الإيجار

الهيئة السعودية تبدي وجهة النظر حول "تعريف عقد الإيجار- حقوق الاستبدال" في المعيار الدولي للتقرير المالي 16

نشرت لجنة التفسيرات الدولية التابعة لمجلس المعايير الدولية للمحاسبة قراراً مبدئياً بشأن تعريف عقد الإيجار عندما يكون للمؤجر حق استبدال الأصل المؤجر خلال مدة عقد الإيجار، وطلبت رأي العموم بشأن هذا القرار.

مجلس معايير المحاسبة في الهيئة يعقد اجتماعه الدوري ويعتمد عدداً من التحديثات على المعايير المعتمدة

عقد مجلس معايير المحاسبة في الهيئة السعودية للمراجعين والمحاسبين اجتماعه الدوري برئاسة رئيس المجلس الأستاذ/ جهاد بن محمد العمري وتم خلال الاجتماع مناقشة عدد من المواضيع المعروضة على جدول الأعمال

تحديث IFRIC لشهر نوفمبر 2022

تحديث IFRIC هو ملخص للقرارات التي توصلت إليها لجنة تفسيرات المعايير الدولية لإعداد التقارير المالية (اللجنة) في اجتماعاتها العامة.

رسالة ماجستير: مدى التزام شركة الخطوط الجوية الكويتية بتطبيق المعيار المحاسبي الدولي 17 - محاسبة عقود الإيجار

هدفت الدراسة إلى التعرف على مدى التزام شركة الخطوط الجوية الكويتية بمتطلبات تطبيق المعيار المحاسبي الدولي 17 الخاص بمحاسبة عقود الإيجار، والتعرف على أهمية وأنواع وميزات وعيوب هذا النوع من التمويل (عقود الإيجار)، حيث تم مراجعة التقرير المالي الخاصة بالشركة لعام 2011 للتعرف على مدى تطبيق بنود المعيار من الناحية المحاسبية وذلك بالاعتماد على منهج (نوعي).

يصدر مجلس معايير المحاسبة الدولية تعديلات ضيقة النطاق على متطلبات معاملات البيع وإعادة التأجير

أصدر مجلس معايير المحاسبة الدولية (IASB) اليوم تعديلات على المعيار الدولي لإعداد التقارير المالية رقم 16 عقود الإيجار، والتي تضيف إلى المتطلبات التي توضح كيفية قيام الشركة بالمحاسبة عن البيع وإعادة التأجير بعد تاريخ المعاملة.

مؤسسة المعايير الدولية لإعداد التقارير المالية تنشر تصنيف IFRS 2021

نشرت مؤسسة المعايير الدولية لإعداد التقارير المالية (IFRS) اليوم تصنيف المعايير الدولية لإعداد التقارير المالية 2021.

معلومات إضافية

-

المحتوى بالإنجليزية

24 March 2021

IFRS Foundation publishes IFRS Taxonomy 2021

The IFRS Foundation has today published the IFRS Taxonomy 2021.

The IFRS Taxonomy enables electronic reporting of financial information prepared in accordance with IFRS Standards. Preparers can use the IFRS Taxonomy to tag disclosures, making them easily accessible to investors who prefer to receive financial information electronically.

The IFRS Taxonomy 2021 is based on IFRS Standards as at 1 January 2021, including those issued but not yet effective.

The IFRS Taxonomy 2021 includes changes to the IFRS Taxonomy 2020 reflecting amended IFRS Standards:

Covid-19-Related Rent Concessions (Amendment to IFRS 16 Leases), issued by the Board in May 2020 (IFRS Taxonomy 2020—Update 1);

Property, Plant and Equipment—Proceeds before Intended Use (Amendments to IAS 16 Property, Plant and Equipment), issued in May 2020 (IFRS Taxonomy 2020—Update 3);

Amendments to IFRS 17 Insurance Contracts and Extension of the Temporary Exemption from Applying IFRS 9 (Amendments to IFRS 4), issued in June 2020 (IFRS Taxonomy 2020–Update 3); and

Interest Rate Benchmark Reform—Phase 2 (Amendments to IFRS 9 Financial Instruments, IAS 39 Financial Instruments: Recognition and Measurement, IFRS 7 Financial Instruments: Disclosures, IFRS 4 Insurance Contracts and IFRS 16 Leases), issued in August 2020 (IFRS Taxonomy 2020—Update 2).

The IFRS Taxonomy 2021 also includes new common practice elements and general taxonomy improvements to support high-quality tagging of:

disclosures related to IAS 19 Employee Benefits (IFRS Taxonomy 2020—Update 5); and

information presented in the primary financial statements (IFRS Taxonomy 2020—Update 4).

Access the files for IFRS Taxonomy 2021 and the supporting information.

تحديث الاجتماع التكميلي لمجلس معايير المحاسبة الدولية مارس 2021

معلومات إضافية

-

المحتوى بالإنجليزية

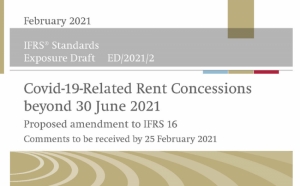

Supplementary IASB Update March 2021—covid-19-related rent concessions

IFRS 16 and covid-19 (Agenda Paper 32)

The International Accounting Standards Board (Board) held a supplementary meeting on 10 March 2021 to:

consider feedback on the February 2021 Exposure Draft Covid-19-Related Rent Concessions beyond 30 June 2021, which proposed an amendment to IFRS 16 Leases; and

redeliberate the project proposal in the light of that feedback.

Feedback and project redeliberations (Agenda Paper 32A)

The Board tentatively decided to finalise the proposal in the Exposure Draft with an additional explanatory transition paragraph.

Ten of 12 Board members agreed with this decision. One Board member was absent.

Due process and permission to ballot (Agenda Paper 32B)

The Board decided to begin the balloting process for the amendment to IFRS 16 without re-exposing it. Twelve Board members agreed with this decision. One Board member was absent.

Twelve Board members confirmed they were satisfied the Board has complied with the applicable due-process requirements to begin the process for balloting the amendment to IFRS 16. One Board member was absent.

Two Board members indicated that they intend to dissent from the amendment to IFRS 16.

Next step

The Board plans to issue the amendment to IFRS 16 on 31 March 2021.

تحديث لجنة تفسيرات المعايير الدولية للتقارير المالية IFRIC لشهر فبراير 2021 متاح الآن

اجتمعت لجنة تفسيرات المعايير الدولية للتقارير المالية في 2 فبراير 2021

معلومات إضافية

-

المحتوى بالإنجليزية

IFRIC Update February 2021

IFRIC Update is a summary of the decisions reached by the IFRS Interpretations Committee (Committee) in its public meetings.

The Committee met on 2 February 2021, and discussed:

Items on the current agenda

Sale and Leaseback of an Asset in a Single-Asset Entity (IFRS 10 Consolidated Financial Statements and IFRS 16 Leases)—Agenda Paper 2

Committee’s tentative agenda decisions

Costs Necessary to Sell Inventories (IAS 2 Inventories)—Agenda Paper 3

Preparation of Financial Statements when an Entity is No Longer a Going Concern (IAS 10 Events after the Reporting Period)—Agenda Paper 4

Other matters

Work in Progress—Agenda Paper 5

Related information

Next scheduled IFRS Interpretations Committee meeting:

16–17 March 2021

Interpretations Committee open items

For further information about IFRS Interpretations Committee activities including how to receive past IFRIC Updates follow the Interpretations Committee group page.

Items on the current agenda

Sale and Leaseback of an Asset in a Single-Asset Entity (IFRS 10 Consolidated Financial Statements and IFRS 16 Leases)—Agenda Paper 2

The Committee considered feedback on the tentative agenda decision discussing the applicability of the sale and leaseback requirements in IFRS 16 to a transaction in which an entity sells its equity interest in a subsidiary that holds only a real estate asset and leases that real estate asset back. The Committee recommended that the Board undertake narrow-scope standard-setting to address this and similar transactions.

Next step

The Board will discuss the Committee’s recommendation at a future Board meeting.

Committee’s tentative agenda decisions

The Committee discussed the following matters and tentatively decided not to add standard-setting projects to the work plan. The Committee will reconsider these tentative decisions, including the reasons for not adding standard-setting projects, at a future meeting. The Committee invites comments on the tentative agenda decisions. Interested parties may submit comments on the open for comment page by 14 April 2021. All comments will be on the public record and posted on our website unless a respondent requests confidentiality and we grant that request. We do not normally grant such requests unless they are supported by a good reason, for example, commercial confidence. The Committee will consider all comments received in writing by 14 April 2021; agenda papers analysing comments received will include analysis only of comments received by that date.

Costs Necessary to Sell Inventories (IAS 2 Inventories)—Agenda Paper 3

The Committee received a request about the costs an entity includes as the ‘estimated costs necessary to make the sale’ when determining the net realisable value of inventories. In particular, the request asked whether an entity includes all costs necessary to make the sale or only those that are incremental to the sale.

Paragraph 6 of IAS 2 defines net realisable value as ‘the estimated selling price in the ordinary course of business less the estimated costs of completion and the estimated costs necessary to make the sale’. Paragraphs 28–33 of IAS 2 include further requirements about how an entity estimates the net realisable value of inventories. Those paragraphs do not identify which specific costs are ‘necessary to make the sale’ of inventories. However, paragraph 28 of IAS 2 describes the objective of writing inventories down to their net realisable value—that objective is to avoid inventories being carried ‘in excess of amounts expected to be realised from their sale’.

The Committee observed that, when determining the net realisable value of inventories, IAS 2 requires an entity to estimate the costs necessary to make the sale. This requirement does not allow an entity to limit such costs to only those that are incremental, thereby potentially excluding costs the entity must incur to sell its inventories but that are not incremental to a particular sale. Including only incremental costs could fail to achieve the objective set out in paragraph 28 of IAS 2.

The Committee concluded that, when determining the net realisable value of inventories, an entity estimates the costs necessary to make the sale in the ordinary course of business. An entity uses its judgement to determine which costs are necessary to make the sale considering its specific facts and circumstances, including the nature of the inventories.

The Committee concluded that the principles and requirements in IFRS Standards provide an adequate basis for an entity to determine whether the estimated costs necessary to make the sale are limited to incremental costs when determining the net realisable value of inventories. Consequently, the Committee [decided] not to add a standard-setting project to the work plan.

Preparation of Financial Statements when an Entity is No Longer a Going Concern (IAS 10 Events after the Reporting Period)—Agenda Paper 4

The Committee received a request about the accounting applied by an entity that is no longer a going concern (as described in paragraph 25 of IAS 1 Presentation of Financial Statements). The request asked whether such an entity:

can prepare financial statements for prior periods on a going concern basis if it was a going concern in those periods and has not previously prepared financial statements for those periods (Question I).

restates comparative information to reflect the basis of accounting used in preparing the current period’s financial statements if it had previously issued financial statements for the comparative period on a going concern basis (Question II).

Question I

Paragraph 25 of IAS 1 requires an entity to prepare financial statements on a going concern basis ‘unless management either intends to liquidate the entity or to cease trading, or has no realistic alternative but to do so’. Paragraph 14 of IAS 10 states that ‘an entity shall not prepare its financial statements on a going concern basis if management determines after the reporting period either that it intends to liquidate the entity or to cease trading, or that it has no realistic alternative but to do so’.

Applying paragraph 25 of IAS 1 and paragraph 14 of IAS 10, an entity that is no longer a going concern cannot prepare financial statements (including those for prior periods that have not yet been authorised for issue) on a going concern basis.

The Committee therefore concluded that the principles and requirements in IFRS Standards provide an adequate basis for an entity that is no longer a going concern to determine whether it prepares its financial statements on a going concern basis.

Question II

Based on its research, the Committee observed no diversity in the application of IFRS Standards with respect to Question II—entities do not restate comparative information to reflect the basis of preparation used in the current period when they first prepare financial statements on a basis that is not a going concern basis. Therefore, the Committee has not [yet] obtained evidence that the matter has widespread effect.

For the reasons noted above, the Committee [decided] not to add a standard-setting project on these matters to the work plan.

Other matters

Work in Progress—Agenda Paper 5

The Committee received an update on the current status of open matters not discussed at its meeting in February 2021. - البلد الأردن

دعوة للحصول علي أوراق بحث أكاديمية لمؤتمر 2022 المشترك

يسعى كل من IASB وFASB و The Accounting Review إلى الحصول على أوراق بحث أكاديمية لمؤتمر 2022 المشترك

معلومات إضافية

-

المحتوى بالإنجليزية

10 February 2021

IASB, FASB and The Accounting Review seek academic research papers for joint 2022 conference

The International Accounting Standards Board (IASB), the Financial Accounting Standards Board (FASB) and The Accounting Review (TAR) have issued a joint call for academic research papers on how key standards are performing in the capital markets. Selected papers will be presented at a joint conference titled Accounting for an Ever-Changing World, currently scheduled for 2-4 November 2022 in New York City, and will be considered for publication in TAR (a publication of the American Accounting Association).

The initiative is intended to strengthen connections between the academic and standard-setting communities and encourage academic research that supports the FASB and the IASB in their post-implementation review of recent major standards.

Call for research papers

Research papers should focus on the effectiveness of the FASB's and/or IASB's standards on revenue recognition (Topic 606 and IFRS 15 Revenue from Contracts with Customers), leases (Topic 842 and IFRS 16 Leases), and financial instruments (Topic 326, Financial Instruments–Credit Losses and IFRS 9 Financial Instruments). Specifically, the standard-setting Boards seek information on whether the standards have:

accomplished their stated objectives;

provided benefits to users of financial information;

resulted in unexpected implementation or continuing application costs; or

given rise to unexpected economic consequences.

Research that examines the impact of similarities or differences between US GAAP and IFRS Standards in these areas is also appropriate.

Find the call for papers here.

Deadline for paper submissions

The deadline to submit papers is 15 May 2022; early submission is encouraged. Selected papers will be presented at the conference and considered for potential publication in TAR. Papers should follow TAR’s editorial policy and be submitted via the journal homepage, along with a cover letter indicating the submission is for the joint conference. (A submission fee of $200 is required and can be paid during submission to the journal).

More information can be found on the conference website.

مجلس معايير المحاسبة الدولية (IASB) يقترح تقديم الدعم للمستأجرين للمحاسبة عن امتيازات الإيجار المتعلقة بـ covid-19

نشر مجلس معايير المحاسبة الدولية للتشاور اقتراحًا لتمديد فترة تطبيق التعديل على المعيار الدولي لإعداد التقارير المالية رقم 16

معلومات إضافية

-

المحتوى بالإنجليزية

IASB proposes to extend support for lessees accounting for covid-19-related rent concessions

The International Accounting Standards Board (Board) has today published for consultation a proposal to extend by one year the application period of the amendment to IFRS 16 Leases issued in 2020 to help lessees accounting for covid-19-related rent concessions.

The original amendment was issued in May 2020 to make it easier for lessees to account for covid-19-related rent concessions, such as rent holidays and temporary rent reductions, while continuing to provide useful information about their leases to investors. The practical relief currently applies to rent concessions that reduce only lease payments due on or before 30 June 2021.

In response to calls from stakeholders and because the covid-19 pandemic is still at its height, the Board proposes to extend the relief to cover rent concessions that reduce only lease payments due on or before 30 June 2022.

The Trustees of the IFRS Foundation have approved a shorter-than-normal comment period of 14 days for this consultation due to the urgent nature of the proposal.

The deadline for submitting comments on the Exposure Draft Covid-19-Related Rent Concessions beyond 30 June 2021 (Proposed amendment to IFRS 16) is 25 February 2021.