عرض العناصر حسب علامة : فيروس كورونا

الثلاثاء, 24 مايو 2022 07:19

إنفوجرافيك.. مستقبل التسويق المحاسبي هو الإستراتيجية

نشر في

إنفوجرافيك

موسومة تحت

الأربعاء, 28 سبتمبر 2022 12:21

مجلس معايير المحاسبة الدولية (IASB) يقترح تقديم الدعم للمستأجرين للمحاسبة عن امتيازات الإيجار المتعلقة بـ covid-19

نشر مجلس معايير المحاسبة الدولية للتشاور اقتراحًا لتمديد فترة تطبيق التعديل على المعيار الدولي لإعداد التقارير المالية رقم 16

معلومات إضافية

-

المحتوى بالإنجليزية

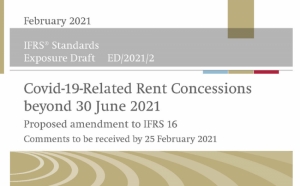

IASB proposes to extend support for lessees accounting for covid-19-related rent concessions

The International Accounting Standards Board (Board) has today published for consultation a proposal to extend by one year the application period of the amendment to IFRS 16 Leases issued in 2020 to help lessees accounting for covid-19-related rent concessions.

The original amendment was issued in May 2020 to make it easier for lessees to account for covid-19-related rent concessions, such as rent holidays and temporary rent reductions, while continuing to provide useful information about their leases to investors. The practical relief currently applies to rent concessions that reduce only lease payments due on or before 30 June 2021.

In response to calls from stakeholders and because the covid-19 pandemic is still at its height, the Board proposes to extend the relief to cover rent concessions that reduce only lease payments due on or before 30 June 2022.

The Trustees of the IFRS Foundation have approved a shorter-than-normal comment period of 14 days for this consultation due to the urgent nature of the proposal.

The deadline for submitting comments on the Exposure Draft Covid-19-Related Rent Concessions beyond 30 June 2021 (Proposed amendment to IFRS 16) is 25 February 2021.

نشر في

محاسبة و مراجعة

الأربعاء, 10 فبراير 2021 14:36

المحاسبة الحكومية عند مفترق طرق: الفرص الناشئة خلال COVID-19

أصبحت المحاسبة الحكومية والتقارير المالية على مفترق طرق اليوم

معلومات إضافية

-

المحتوى بالإنجليزية

Government accounting at crossroads: Emerging opportunities during COVID-19

ED OLOWO-OKERE|FEBRUARY 05, 2021

Government accounting and financial reporting are at a crossroads today. Providing information on how much cash is received into treasuries and paid out for goods, services and transfers is not enough. Stakeholders are demanding more accountability and engagement in public finances. Governments are spending large sums of money to tackle the health emergency and to implement massive fiscal stimulus programs in response to the pandemic. Undoubtedly, timely and quality information is necessary to better assess the financial health of governments and to communicate the financial consequences of the pandemic to all stakeholders. This can contribute to building the much-needed trust in governments and improve the effectiveness of their pandemic response.

The World Bank’s recent paper on the role of Government Financial Reporting in times of the COVID-19 Pandemic provides guidance to accountants and auditors on identifying opportunities to improve financial reporting within the existing systems. The paper also highlights the impact of the pandemic on government financial performance, position and cash flows.

Similarly, the International Public Sector Accounting Standards (IPSAS) Board and International Federation of Accountants (IFAC) released a COVID-19 Intervention Assessment Tool, which helps assess, evaluate and inform various types of interventions by governments. Another recent study by the Association of Chartered Certified Accountants (ACCA) on Sustainable Public Finances through COVID-19 highlighted the critical need to record and manage the assets and liabilities being created through the below-the-line policy measures, such as guarantees and equity injections.

Some of the emerging lessons on government financial reporting during the COVID-19 crisis include the following:

Financial statements information has been traditionally underutilized by governments. Going forward, balance sheet information can inform how to achieve an inclusive and sustainable recovery in the post COVID-19 world.

Government accountants should more proactively demonstrate the value of financial statement information and why it should be analyzed in conjunction with statistical information.

While ‘accrual basis accounting’ is necessary to prepare financial statements that provide a comprehensive overview of the impact of COVID-19, jurisdictions following ‘cash basis accounting’ can enrich their financial statements with supplementary information for better decision making.

Comprehensive financial statements based on accrual-based accounting will contribute to debt transparency and improved decision making. For example, in the current situation where global public debt is projected to approach a record high in 2021, countries need to closely monitor their sources of funding and associated costs. Comprehensive financial statement information on debt is especially useful for making policy decisions.

Annual and interim financial statements should be prepared on a timely basis in order for them to be useful to policy makers and help inform pandemic-related response financial decisions.

Countries need to accelerate implementation of accrual-based accounting and financial reporting reforms, preferably aligned with the International Public Sector Accounting Standards (IPSAS) , to have more comprehensive and reliable financial information for decision making.

Ministries of Finance need to ensure that the necessary systems and procedures, including Integrated Financial Management Information Systems (IFMIS) implementation, are in place to facilitate the recording of transactions and preparation of financial statements. These include consolidated ones with different levels of aggregation and even the whole-of-government financial statements where feasible

Financial statements that include information on the long-term fiscal sustainability, with a focus on the impact of the pandemic, are necessary.

Strong coordination by the Ministry of Finance and Accounting Agencies with the auditors of government financial statements, i.e. Supreme Audit Institutions (SAIs), is critical. This is not only with respect to the preparation of audited financial statements but also in developing and implementing accounting and financial reforms such as migration to accrual-based accounting.

Accounting and auditing agencies should regularly conduct business continuity assessments so that governments are ready to face future emergencies without detrimental effects on their operating capacity , and that essential and non-essential staff can work remotely when needed.

The COVID-19 pandemic has changed the world and how governments operate forever. By strengthening public financial management systems and protocols today, governments will be better prepared for an increasingly uncertain tomorrow.

نشر في

موضوعات متنوعة

الثلاثاء, 23 نوفمبر 2021 12:03

التحديث التكميلي لمجلس معايير المحاسبة الدولية (IASB) فبراير 2021 -امتيازات الإيجار ذات الصلة بفيروس كورونا

ناقش مجلس معايير المحاسبة الدولية IASB امتيازات الإيجار المتعلقة بـ covid-19 في اجتماع مجلس الإدارة التكميلي في فبراير 2021

معلومات إضافية

-

المحتوى بالإنجليزية

IASB discusses covid-19-related rent concessions at supplementary February 2021 Board meeting

The Board decided at a supplementary meeting on 4 February 2021 to propose an extension to the time period over which the practical expedient in paragraph 46A of IFRS 16 Leases is available for use.

A project has been added to the Board’s work plan on the proposed amendment. Those with an interest can follow developments in the project by registering for alerts. The Board expects to publish the proposed amendment in an exposure draft on 11 February 2021 with a 14-day comment period.

The IFRS Foundation Trustees, responsible for governance and oversight of the Board, have approved the 14-day comment period. The Due Process Handbook sets out that 75% of the Trustees must approve comment periods shorter than 30 days.

A full summary of the Board’s supplementary meeting is available in the Supplementary IASB Update February 2021—covid-19-related rent concessions. - البلد الأردن

نشر في

محاسبة و مراجعة

موسومة تحت

الأحد, 07 فبراير 2021 12:49

هل بيانات شركتك آمنة؟

يبدو أنه لا يمر يوم دون أنباء عن اختراق الشبكات والبيانات

معلومات إضافية

-

المحتوى بالإنجليزية

Is your firm's data safe?

By Ted Needleman

January 29, 2021, 9:00 a.m. EST

11 Min Read

Facebook

Twitter

LinkedIn

Email

Show more sharing options

It seems like not a day goes by without news of networks being breached and data hacked. One of the most recent, the SolarWinds hack, led to breaches within multiple areas of our government, while individual ransomware attacks on vital parts of our economy, including entire towns and hospitals, are being reported more and more frequently.

Given the chaos that the COVID-19 pandemic has caused through 2020, and with no quick resolution in sight, the last thing you need is for your practice to be hacked or held for ransom. But the plain truth of the matter is that the need to work remotely, fueled by the coronavirus, has made your practice and your clients more vulnerable than they were in the past.

“The rash of lucrative ransomware attacks over the past year pointed to organized hacker groups specifically targeting medical, legal and accounting businesses where they could not only invoke the ransom but also steal a treasure trove of client/business information,” said Roman Kepczyk, director of firm technology strategy at Right Networks. “This allowed the hackers to threaten to release confidential client information or intellectual property if the ransom was not paid. In addition to using the personally identifiable information to fraudulently file tax returns and instigate identity theft, in some instances the hackers contacted clients of the firms for further extortion, threatening to release confidential, compromising or embarrassing information.”

Article Managing Cash Flow– a Critical Factor to Small Business Success

Your small business clients are a key pillar of the U.S. economy, providing income to their families and delivering growth and innovation to the...

PARTNER INSIGHTS

SPONSOR CONTENT FROM CHASE INK

Obviously, protecting your systems and data from outside intrusion is important. But even more important is protecting your clients’ systems and data. And the fact that many of us are working from home, and will likely continue to do so, at least part-time, for the foreseeable future, only increases the risk of exposure.

The steps you can take range from very basic to ultra-sophisticated. Your first lines of defense are great backup procedures and using a good anti-malware application. But these are just the beginning. You need to take active measures to protect your systems, whether they are in your physical office, or your office on the kitchen table.

It takes two

Two of the most common and easiest security measures to implement are two-factor authentication and encryption. While two-factor authentication can be a bit annoying, having to enter both a password and a verification code sent to an email account or messaged to a mobile account significantly reduces the chances of a breach if someone is able to get hold of your password.

Stronger passwords with greater security are also a must. Too many are still using weak passwords such as the names of their spouses, children or dogs, or even “Password123.” Many remote applications are now insisting on stronger passwords containing upper- and lower-case letters, numbers and special symbols. But keeping track of these, especially when they are different for every application, is a major concern for many users. If this is the case with your practice, there are several ways you can use difficult-to-guess passwords and still not have to write them down to remember what they are for each application.

The most common of these is to use a password manager that tracks your passwords and inserts the proper difficult-to-remember password into the appropriate application. Popular password managers include 1Password and LastPass, but there are plenty of similar applications for PCs, Macs, smartphones and tablets.

Another alternative is to use a hardware authentication key that plugs into a USB-A oe USB-C port or provides NFC (near field connectivity — the technology used in tap-and-pay credit cards and some phones) to work with mobile devices that incorporate this feature. One popular key is offered by Yubico, though they are far from the only vendor.

“The YubiKey provides users with a hardware-backed strong multifactor authentication solution that has a proven track record for protecting accounts,” Chad Thunberg, chief information security officer at Yubico, told us. “Not every service provider or application — including some of the popular accounting software suites — have yet adopted the FIDO [Fast IDentity Online] authentication standards that we use for the YubiKey. However, many of these applications support using a single sign-on [SSO] identity provider that does support the use of YubiKeys. To get started, users can enroll their YubiKey with their favorite identity provider (e.g., Google, Apple or Microsoft) and then use that identity provider to log onto their accounting software. I took a brief look at some of the popular offerings, and FreshBooks, QuickBooks Online and Sage Accounting all support SSO.”

Encryption is yet another option that you should be aware of. Richard Kanadjian, encrypted USB business manager at Kingston Technology, pointed out that, “Encryption basically means that if you encrypt the data on that USB drive and you lose it, the probability that somebody can actually retrieve that data is actually infinitesimal. It’s actually almost zero. And the reason is we have password controls. For example, you have a password or a pin for your USB drive and our encrypted drive will only let you enter the password 10 times. So, if you enter it more times and if somebody’s guessing, the drive will literally wipe its contents and erase the data. You will actually not have any data to be exposed to a breach.”

Keeping the data for your applications on an encrypted drive is a usable approach, but keep in mind that the data on an encrypted drive should be backed up to a secure location, be it the cloud or a second encrypted drive, just in case the encrypted drive containing important data is lost or stolen.

You should also be very aware of where you are using your laptop. Too many people go down to the local coffee shop or library, where the internet is freely available, and don’t take reasonable precautions against infections and intrusions. Infecting the routers at these locations with malware is becoming very common, and the compromised internet at these locations can infect hundreds or even thousands of the systems being used there, as well as any networks that the infected systems are then attached to.

“One of the biggest concerns that we are seeing is so many employees were forced to work from home and all of a sudden they’re sitting on networks that are outside of the control of corporate IT,” Stephen Lawton, special projects editorial director at SC Media, pointed out. “If you let the employee simply use their home systems and their home networks without any IP control, quite frankly what you’re going to get is BYOD — not ‘Bring your own device,’ but ‘Bring your own disaster.’ The lack of security controls on most home networks is really quite astounding. Many people have never updated the firmware and their routers. They’ve never put any kind of security controls or software on their systems. If you’re going to have your workers working from home, the practice really needs to invest in laptops specifically for that purpose, that have security controls built into them. At the minimum you need some enterprise-class antivirus, anti-malware anti-ransomware software. You should also have the systems going over a virtual private network back to a home base. VPNs are certainly not foolproof, but they’re better than not having anything at all, or just going through the employee’s personal network.”

© Pedro Nunes/pn_photo - stock.adobe.com

Your face and your printer

Biometrics as a password substitute are also becoming increasingly common. No, you don’t have to have a retina scanner mounted on your PC or laptop, though it would hardly be surprising to see something along those lines using the almost-ubiquitous webcam in the near future. But while retinal scanners have been around for years, along with the handprint readers often seen in movies, they are pretty much relegated to very high security installations with equally high security budgets and resources.

But real, usable, biometric roadblocks to unauthorized network and device penetration have been available for years. Fingerprint readers, especially in laptops, are common these days. And both the iOS and Windows operating systems have facial recognition capabilities that can not only serve as an alternative to system passwords, but in many cases can also be used as passwords to sensitive applications such as bank and credit card accounts.

This is a handy inroad to your sensitive systems and applications, but is somewhat blunted by the fact that most of the facial recognition capabilities at the entry level, such as those included in the operating system, require that the entire face be visible to provide authentication. Wearing a mask, a necessity out in public or in your office these days, often defeats this handy sign-in method.

One area of vulnerability that’s been getting more attention recently are devices connected to the Internet of Things — components, such as printers and multifunction printers, that are connected to your network and also have their own pathways into the internet. Most of us are familiar with threats such as phishing and embedded malware, but there is another route into your network that you may have not considered.

“A lot of times the network perimeter has, in the past, been used as a way to secure devices.” Shivaun Albright, chief technologist of print security at HP, pointed out. “And in this day and age, with email, phishing attacks, clicking on something, any type of email or link, you cannot guarantee that your interior perimeter network is secured. You just can’t. And one of the things that we’ve seen, in fact last year, was an article from Microsoft in August of 2019. They had highlighted that they had caught Russian state hackers using IoT’s breached networks. And, by the way, they found that devices that had been hacked were Voice over IP phones and office printers.”

Clients are targets, too

There’s obviously a lot more to look at security-wise than what is covered here. And, as with many aspects of technology, IT security is a moving target — what’s true and secure today might be vulnerable tomorrow. Developing the expertise and knowledge to deal with the new threats that emerge every day is not only an ongoing process, but one that can be difficult to maintain and expand, which is yet another good reason to examine the practices and protocols in place in your practice and at your clients’.

Protecting your and your clients’ data is not only a fiduciary responsibility, it’s also good business practice. “Firms that have been breached will not only have to deal with a damaged reputation, but can expect to see client churn and having to deal with ongoing litigation from clients that were impacted,” warned Kepczyk.

It takes time and money to build expertise in this area. And even after an extensive immersion in security, it’s likely that you still might not have the experience to know just how to determine where your practice’s vulnerabilities are and how to address them when you do discover them.

One approach suggested by Randy Johnston, executive vice president of K2 Enterprises, that is especially applicable if you outsource some or all of your IT support, is to “choose reputable IT providers that understand and implement best practices for security to help your internal IT staff. While security risks morph over time, the provider must actively respond to new threats and continuously adjust their security protocols and technical setup to protect your firm.”

And Kepczyk added, “Employee training is critical, particularly in regards to phishing threats, which account for the entry of the vast majority of breaches, so we suggest you outsource that to third parties such as KnowBe4, PhishMe, Wombat Security, etc., that will do phishing testing and employee training.”

If you’re thinking of expanding your practice into this growing area of concern, or just want to better educate yourself, Jim Bourke, a partner and managing director of advisory services at Top 100 Firm WithumSmith+Brown, has a few suggestions on getting started. To start, “I would highly recommend getting your hands on the AICPA cybersecurity risk management reporting framework.”

Bourke added, “I would discuss the AICPA’s ‘SOC for Cybersecurity’ engagement with your clients. At Withum, we are all over that space. As CPAs, only we can issue a ‘SOC for Cybersecurity’ report! There is huge demand for this type of deliverable today. The AICPA has classes and workshops in this space, allowing any CPA to gain the knowledge and expertise that they need to perform these services.”

But whether or not you decide to add security consulting to your practice or partner with a company that has expertise and reputation in that area, keep in mind that the very last thing you want to tell a client is that you had a data breach, were hacked, or that your system is locked due to ransomware. A good backup strategy is a necessary first step, but where you go from there is going to determine just how secure your ongoing livelihood is going to be. And while there is no such thing as perfect security, you need to be aware of where you are vulnerable, and take steps to strengthen those areas of your procedures and practices.

نشر في

تكنولوجيا المعلومات

موسومة تحت

الأربعاء, 03 فبراير 2021 15:16

دعوة للترشيح في اللجنة الاستشارية لأسواق رأس المال

تبحث اللجنة الاستشارية لأسواق رأس المال عن مرشحين جدد للانضمام إلى CMAC

معلومات إضافية

-

المحتوى بالإنجليزية

CMAC—Call for members

The Capital Markets Advisory Committee (CMAC) is seeking new candidates to join the CMAC from 1 January 2022 for a term of three years, renewable once for a further three years. The CMAC welcomes applications from analysts and investors from all over the world. CMAC members are drawn from a variety of industry and geographical backgrounds and are selected by the CMAC on the merits of their professional competence as capital market participants using financial reporting information and their ability to represent capital market participants' views.

CMAC

The CMAC is an independent advisory body established with the specific aim of providing regular input from an international community of users of financial statements to the International Accounting Standards Board (Board). The Board develops IFRS® Standards, which are required for use by companies in more than 100 countries, including two-thirds of the G20.

The purpose of the CMAC is to represent to the Board the perspectives of professional capital market participants who are users of financial reporting information, such as analysts, investors and ratings agencies. It seeks to be broadly representative of both industries and geographic regions and of both equity and credit asset classes to offer articulate reasoned and diversified viewpoints.

As such, the CMAC consists of up to 20 members with extensive practical experience in analysing financial information. They do not represent the views and interests of their affiliations, except where explicitly stated. Information about the CMAC’s current members is available here.

The CMAC meets with Board representatives during its one-day meetings that take place three times a year. In response to the impact of the coronavirus (covid-19) pandemic, we have replaced in-person meetings with virtual meetings. We provide digital access to meetings, and we provide regular updates on specific meeting arrangements. Members receive meeting papers for review in advance of each meeting.

Apply

Please indicate your interest by emailing the Investor Engagement team, including a cover letter and brief curriculum vitae.

Any personal data supplied to the IFRS Foundation by you will only be used for this application process for CMAC Candidate selection. The IFRS Foundation will retain such data no longer than is necessary for that purpose, and in accordance with its data retention policy and all applicable data protection laws.

If you have any questions in relation to the above contact the Investor Engagement team.

نشر في

موضوعات متنوعة

موسومة تحت

الأربعاء, 28 سبتمبر 2022 12:07

أهمية المعايير الدولية وملاءمتها: التركيز على الأخلاق والاستقلالية

كانت التحديات الاقتصادية والاجتماعية والبيئية العالمية تختبر الأفراد والعائلات والمنظمات والسوق المالي، وبالتالي مهنة المحاسبة

معلومات إضافية

-

المحتوى بالإنجليزية

The Importance and Continued Relevance of International Standards: A Focus on Ethics and Independence

DIANE JULES, SARAH GAGNON

Global economic, social, and environmental challenges have been testing individuals, families, organizations, the financial market, and in turn, the accountancy profession. And that was before the COVID-19 pandemic.

In response, professional accountants must now be vigilant of the heighted risks that will arise out of the pandemic and continue to ensure that their actions are anchored by the fundamental principles of integrity, objectivity, professional competence and due care, confidentiality, and professional behavior set out in the International Ethics Standards Board for Accountants’ International Code of Ethics for Professional Accountants (including International Standards) (the Code). Similarly, the important role that professional accountancy organizations (PAOs), national standards setters, accountancy educators, and in some cases, regulators play in supporting accountants in complying with the Code cannot be overstated.

The Role of an International Code of Ethics

The international business community has expressed the need for a single set of international standards which enhances consistency and quality of services provided by professional accountants, strengthens financial stability and public confidence, and reduces regulatory fragmentation across borders. Businesses, governments, and other organizations rely on and place confidence in accountants’ work because of their commitment to act ethically and in the public interest. The Code requires accountants to comply with five fundamental principles of ethics. These principles promote the standard of behavior expected of individual accountants and firms and help orient their public interest mindset.

Upholding the public interest is a long-standing responsibility of accountants irrespective of their roles, and that is ultimately the bedrock of public trust in the profession.

Compliance with the Code in preparing, presenting, and auditing financial information is key to preserving public trust and mitigating fallouts during times of crisis, including during the COVID-19 pandemic. However, for the Code to continue to meet its intended purpose, it must be adopted, implemented, and enforced. PAOs play a key role in the adoption of international standards, including the Code.

A Recap of Revisions and Restructured Changes to the Code

The Code set out in the IESBA 2018 Handbook has been effective since June 2019 and is significantly revised and restructured from previous versions that jurisdictions may have already adopted (e.g., the 2016 version or even 2009).

Key changes include:

An enhanced and more prominently featured conceptual framework—the universal approach that all accountants are required to apply to identify, evaluate and address threats to compliance with the fundamental principles that might arise when undertaking professional activities.

Clearer and more robust provisions pertaining to safeguards that are better aligned to the specific threats.

Strengthened independence provisions addressing the long association of personnel with an audit or assurance client.

New and revised sections dedicated for professional accountants in business (PAIBs) relating to:

Pressure to breach the fundamental principles; and

Preparing and presenting information.

Clear guidance for professional accountants public practice (PAPPs) that relevant PAIB provisions set out in Part 2 of the Code are applicable to them.

Strengthened provisions for PAIBs and PAPPs relating to offering or accepting inducements, including gifts and hospitality.

New application material to:

Emphasize the importance of understanding facts and circumstances when exercising professional judgment (PJ).

Explain how compliance with the fundamental principles supports the exercise of professional skepticism (PS) in an audit or other assurance engagements.

Package the non-compliance with laws and regulations (NOCLAR) provisions which came into effect in July 2017 in a restructured format.

Include a glossary of defined terms and key concepts.

Recent and Upcoming Revisions

Because of the fluid and dynamic nature of the environment in which accountants operate, it is necessary to continually review the relevance and impact of the Code to ensure that it remains fit for purpose. It is against this backdrop that the IESBA developed its 2019-2023 Strategy and Work Plan (SWP).

Since the release of the 2018 Handbook, the IESBA has finalized the following changes to the Code:

Alignment of Part 4B to ISAE 3000 (Revised). Part 4B comprises the independence provisions for assurance engagements other than audit and review engagements. The revisions to Part 4B of the Code are to reflect terms and concepts used in the IAASB’s ISAE 3000 (Revised) and were developed in close coordination with the IAASB. The final pronouncement was released in January 2020 and will come into effect in June 2021. Early adoption is permitted.

Role and Mindset Expected of Professional Accountants. The final pronouncement with revisions to promote the role and mindset expected of professional accountants was released in October 2020. The revisions reaffirm the accounting profession’s responsibility to act in the public interest and the fundamental role of the Code in meeting that responsibility. Among other matters, the revisions:

Raise behavioral expectations of all professional accountants and require them to have an inquiring mind as they undertake their professional activities.

Emphasize the need for accountants to be aware of the potential influence of bias in their judgments and decisions.

Highlight the supportive role that organizational cultures can play in promoting ethical conduct and business.

The role and mindset revisions will come into effect in December 2021. Early adoption is permitted.

Objectivity of an Engagement Quality Reviewer (EQR). The IESBA approved a new section of the Code providing guidance to address the objectivity of an EQR based on the conceptual framework in September 2020. The EQR final pronouncement was released on January 14, 2021. It will be effective for audits of financial statements for periods beginning on or after December 15, 2022. Early adoption will be permitted.

The IESBA’s EQR project was closely coordinated with the International Auditing and Assurance Standards Board (IAASB) in the context of the IAASB’s project to develop International Standard on Quality Management (ISQM) 2, Engagement Quality Reviews, which was released in December 2020.

Non-Assurance Services (NAS) and Fees. The IESBA approved revisions to strengthen its International Independence Standards with respect to its NAS and fee-related provisions in December 2020. Subject to the Public Interest Oversight Board’s, the final pronouncements will be released by May 2021 and will be effective for audits of financial statements for periods beginning on or after December 15, 2022. Early adoption will be permitted.

IFAC’s Role in Adoption and Implementation of the Code

Resulting from the collaborative approach that IESBA and IFAC has taken in relation to awareness raising, stakeholder outreach and adoption and implementation support, many jurisdictions either have adopted, or have stated plans to consider adopting, the more robust 2018 edition of the Code. It is important that this momentum continue.

IFAC membership requires a commitment of PAOs to use their authority and influence to adopt the international standards and best practices in their jurisdictions. IFAC member organizations around the world are required to adopt and implement ethics standards, including independence requirements, that are no less stringent than those in the IESBA Code. If law, regulation, or national ethics standards differ from or go beyond those set out in the IESBA Code, accountants need to be aware of these differences and comply with the more stringent provisions unless prohibited by law or regulation. This means that national standard setters can include additional or more stringent provisions to meet the needs of their local jurisdictions.

PAOs that are not authorized to adopt the Code have an essential role in raising awareness of the importance of adopting the most current version of the Code. Further, all PAOs have an important role in educating accountancy professionals and relevant stakeholders about the revisions that are periodically made to international standards, including the Code. This aids in developing jurisdiction-specific implementation support to foster the right cultures within organizations and broader business communities to help professional accountants apply the Code’s requirements.

Status of Adoption of International Standards, including the Code

IFAC members regularly report on the status or progress of their adoption efforts. This makes IFAC well-positioned to maintain, monitor, and report unique information related to the global adoption status of international standards, including the Code. It also helps IFAC facilitate greater engagement and enhanced collaboration among stakeholders in the accountancy profession. IFAC’s 2019 International Standards Global Status Report represented the first baseline for global adoption status and also outlines the different adoption approaches and procedures. For the majority of jurisdictions, adoption of international standards takes a significant amount of time and resources. The process typically involves extensive local stakeholder consultations, coalition-building, and advocacy. In some jurisdictions, there is also additional time needed to translate the standards as part of the adoption process.

Has your jurisdiction adopted the latest Code of Ethics? Explore on IFAC’s Global Impact Map.

All of these nuances contribute to our immense pride in celebrating that more than 80 of the 134 IFAC member jurisdictions have either already adopted or have stated plans to adopt the 2018 Code! In addition, the Forum of Firms—an independent association of international networks of accounting firms—adopt policies and methodologies that align to the IESBA Code when performing transnational audits.

Looking Forward

The 2018 edition of the Code provides a solid foundation to preserve the relevance and public-interest focus of the global accountancy profession. We encourage stakeholders in jurisdictions that have not started the adoption process to do so now.

نشر في

محاسبة و مراجعة

الأربعاء, 27 يناير 2021 15:18

هل تتلاشي فرص التعافي السريع وسط عودة ظهور COVID-19؟

يرى المحاسبون أن فرص التعافي السريع تتلاشى

معلومات إضافية

-

المحتوى بالإنجليزية

Accountants see chances of swift recovery slipping away

By Michael Cohn

Accountants around the world are seeing the prospects for swift economic recovery slipping away amid a resurgence in COVID-19.

The latest edition of the quarterly Global Economic Conditions Survey from the Association of Chartered Certified Accountants and the Institute of Management Accountants found that confidence fell in North America in the fourth quarter of 2020, after surging in the third quarter. On the other hand, there was a big improvement in confidence in the Middle East, perhaps due to a rebound in oil prices. More than 50 percent of the accountants who responded to the survey in the Asia Pacific region, North America and South Asia expect sustainable recovery in the second half of this year.

Expectations for an economic recovery rose late in 2020 as pharmaceutial companies began producing coronavirus vaccines, but the slow pace of the rollout due to manufacturing and distribution delays is likely to dampen optimism further. Accountants report that the companies and firms where they work anticipate pent-up demand for products and services once vaccines are widely available and people are able to travel more freely, although the mutating strains of the virus are adding uncertainty to those prospects.

Health care workers test people at a COVID-19 testing site in the parking garage for the Mahaffey Theater in St. Petersburg, Florida.Eve Edelheit/Bloomberg

“Last year was the worst for the global economy for several decades,” said Warner Johnston, head of ACCA USA, in a statement Tuesday. “2021 will see recovery, but precisely when and how strong it will be is very uncertain. We anticipate a weak start, followed by a recovery gathering momentum through the second half. Much depends on the evolution of the COVID virus and variants relative to the progress of vaccination programs, and there is great uncertainty surrounding these developments.”

Confidence among accountants fell in the ACCA and IMA’s Q4 survey, after jumping by the greatest percentage on record in Q3. Orders and capital spending showed little change in Q4 and remained well below their pre-crisis levels of a year ago. Employment recovered significantly in Q4 on the index, thanks to a relatively good jobs market rebound since the early weeks of the pandemic. Overall, the survey indicates expectations among accountants for continued economic recovery in early 2021.

Concerns and fears about customers and suppliers going out of business edged lower worldwide in Q4 but remain elevated, highlighting the extreme uncertainty in the global economic outlook at the beginning of 2021. More than half of the respondents in Asia Pacific, North America and South Asia expect sustainable recovery in the second half of this year.

However, in many parts of the world, the likelihood of a swift recovery is dim for this year, especially where the vaccine rollout has barely begun at all.

“The pandemic has forced millions into extreme poverty as emerging markets suffered recession for the first time in decades last year,” said IMA vice president of research and policy Raef Lawson in a statement. “Policy responses to the pandemic have left the public finances of most economies in a perilous state with budget deficits in the range of 10 percent to 15 percent of GDP in many countries with debt to GDP ratios well over 100 percent.”

In Africa, for example, the renewed rises in infections toward the end of 2020, along with a continuing absence of foreign tourists, point to a weak start to 2021. The declining amount of GDP per capita across the region, according to the World Bank, will push tens of millions of people into extreme poverty.

نشر في

موضوعات متنوعة

موسومة تحت

الأربعاء, 20 يناير 2021 13:03

فتح الصندوق الأسود للذكاء الاصطناعي

وصف في السبعينيات من القرن الماضي أستاذ الروبوتات في طوكيو ماساهيرو موري، كيف تبدو الآلات أكثر شبهاً بالإنسان

معلومات إضافية

-

المحتوى بالإنجليزية

AI, applied: Opening the black box

By Ranica Arrowsmith

There’s a phrase for the uneasiness many of us feel when confronted with humanlike machines — the Uncanny Valley. Coined in the 1970s by Tokyo robotics professor Masahiro Mori, the phrase describes how as machines appear more humanlike, they become more appealing to humans — but only up to a point. After that, as they appear more humanlike but not quite, they inspire revulsion in the observer.

In the accounting profession, there is a similar uneasiness when dealing with the idea of AI, though it has nothing to with how the software looks. The technology has the potential for high-level automation of processes, ultimately saving a lot of time for the accountant, but with its ability to perform tasks that are traditionally the purview of human beings, does this mean a diminished role for the accountant, or even the loss of jobs?

The good news is, the experts don’t think so.

Justin Adams, whose company Anduin has just launched an AI-enabled accounts receivable platform, insists there is an “art” to billing that must remain in the AR process for it to be meaningful and profitable — the deep knowledge of a client over time, for example, can affect a billing relationship. And Samantha Bowling of Garbelman Winslow CPAs isn’t interested in simply speeding up the audit with AI — she wants to provide an audit of such high quality that it’s unquestionable. These types of service goals can only be achieved by marrying AI with the human professional, with all the professional’s experience, skepticism and emotional intelligence.

Artificial intelligence can have an air of mystery about it, to say nothing of a hint of the unnatural, with something we value as inherently human — intelligence — being created and inserted into something inanimate — a machine.

It makes sense that we feel this way. The programming precursor to what we today call artificial intelligence was neural networks, code that was inspired by and modeled on actual human neural networks in the brain. Today, artificially intelligent programs have the ability to observe patterns and use those to “learn” behaviors and responses, making the technology smarter and more usable over time.

It’s worth bearing in mind the various ways in which AI is already here, working in the background of the accounting and enterprise platforms you know well, automating processes and making software more efficient. All the user sees are the benefits. But the market is now seeing true AI platforms that apply machine learning to entire processes end to end, such as AR/AP. And the common theme among all use cases for such AI-rich platforms is time — the time it takes to adopt the software and to validate it, to train it enough for a firm to realize its benefits. The machine has to learn. This takes an investment both of money and patience, but for the willing, it’s worth it.

Today, artificial intelligence is transforming processes across the accounting profession, for those are ready to invest in and adopt it. It’s not just being practically applied in audit, where AI is being used for data analysis and anomaly detection — we will look at examples of AI transforming AR/AP, as well as explore the implications of AI in sales tax automation.

Accounts: Receivable

Despite … everything about this year, venture capital funding continued on an upward trend in 2020, with the third fiscal quarter bringing in the second highest amount of VC funding per quarter on record. Artificial intelligence is high on the list of hot tech, which makes it no surprise that Anduin was able to obtain seed funding and launch its first AI-powered product suite all during the COVID-19 pandemic.

Anduin co-founders Justin Adams and Pat Morrell have built an AI-driven accounts receivable platform, Intelligence-Based Billing, for accounting firms. The platform launched in December, so it remains to be seen how successful adoption will be, but the pair of entrepreneurs have succeeded before in the AI space. Prior to founding Anduin, Adams and Morrell started, grew and sold a company that made an AI-driven product for the health care space, all within two years. That whirlwind experience propelled them into their current venture, and their success made them attractive prospects for investors.

“We had zero health care background when we started Digitize.AI,” Morrell said. “But we went to CFOs of health care companies and asked them where their biggest pain point was. When they said ‘prior authorizations,’ I had to look it up on Wikipedia — but I knew that a manual process is a manual process, and can be automated.”

Adams and Morrell weren’t quite as clueless entering the accounting space. Adams had spent years working at Big Four firm PwC, first in a consultative capacity and then internally managing technology projects. When they asked accountants what they would change if they could wave a magic wand, accounts receivable was a common answer. The process, managed manually, is scattered and unwieldy, and even streamlined client portals don’t optimize the process for each individual client and their payment habits.

There’s an art to billing, Adams said, and the platform tries to preserve that for the accountant. “Think of it from a client’s perspective,” he said. “There’s tons of friction. It can be confusing. You could have received a service three months earlier, and when you get the invoice, you’re trying to remember what you’re paying for again.”

Intelligence-Based Billing is made up of four modules (which can be bought separately), handling invoicing, collection, payments and internal analytics. The platform automates the invoicing process so bills are sent in a timely manner, but it also learns a client’s payment habits over time. How many emails or messages does it take before an invoice is opened and viewed? How many contacts does it take before a client pays the bill? Each client is different, and therein lies the art. If a client typically pays an invoice after two emails and a phone call, Intelligence-Based Billing will “remember” that over time, optimizing the process for each firm-client relationship.

More “art” that the AI tries to replicate: The analytics feature can be used in part to automate, so to speak, that gut feeling accountants also have to pay attention to when it comes to value-based billing. For instance, Morrell pointed out, a firm may have worked a certain number of hours on a project, but with their sense of the market over the years, they know that a client might expect a certain discount. Each client perceives different aspects of a service as more valuable, and also might need different billing structures to remain a client in the long term. Intelligence-Based Billing pulls and analyzes data from across firm systems to inform this type of decision-making.

“The fundamental pain is the anxiety that firms are leaving money on the table; and that firms don’t have real visibility into their cash flows,” Morrell said. “On the partner level, it’s all about liberating them to focus on complex, creative, value-generating service delivery.”

Intelligence-Based Billing is new on the market, and is signing up “trailblazer firms” now as its first customers. Time will tell how successful it will be, but no matter what, Anduin is part of a small group of innovators bringing fully formed, AI-enabled automation to firms of all sizes, for everyday firm functions, and will help set the stage for what’s to come.

Accounts: Payable

Youngseung Kuk manages business outsourcing services for Top 100 Firm Armanino in Boise, Idaho. This year, Kuk spearheaded the implementation of Vic.ai, a platform that automates the accounts payable process using AI. Using AI to tackle AP for clients was “low-hanging fruit,” Kuk said, as all companies, no matter what type, have bills to pay.

Armanino uses Bill.com firmwide for all AP, so the firm worked with Vic.ai to integrate the software to make the end-to-end AP process more streamlined.

Kuk and his team are validating Vic.ai as they use it, adding clients slowly, one at a time, to make sure they give the program enough time to learn its clients and become highly efficient at its predictions. This is a key part of understanding AI — it takes time.

Software that runs on AI doesn’t operate like the software we’ve become accustomed to. It doesn’t perform an exact set of functions as programmed, and only as programmed. Artificial intelligence learns as it goes, which means that by the end of a certain period of time, the software will operate very differently for each client, each firm, each project.

Kuk estimates it will take Vic.ai three years to predict client behavior and needs at a close-to-perfect rate. The wait is worth it for the sheer amount of time it can give back to an accountant once the AP process for a client is basically fully automated.

Armanino has one client, a law firm, that has highly repetitive bills that don’t have too many complicated dimensions (i.e., company name, address, and so on, are usually in the same spot on the invoices). Within a few months of use, Vic.ai can now predict any given AP workflow for that client with about 80 percent accuracy. If this is true for this client, Kuk said, that’s enough to know it’s possible for the others. Currently, Armanino has 46 clients on Vic.ai, and plans to keep validating the software so it can add more in time.

“The time spent validating is worth it, because by the end, as a firm, we’re going to be so much more scalable,” Kuk said. “Once you free up some capacity, even just from an AP standpoint we can do a number of different things for our clients that add more value, like confirming all vendors have W-9s, for example, or reaching out to vendors proactively if they haven’t accepted an ACH payment. These are just some basic examples, but I think we’re at the tip of the iceberg and nowhere near the full potential of AI.”

“Two years ago, we made an investment in artificial intelligence in a big way. It became part of firmwide strategy,” explained Tom Mescall, partner-in-charge of consulting at the firm. “Most CEOs, CFOs and business operators know the headline of AI, but they don’t know how to apply it in a business setting. We’ve done a lot of work around demystifying AI and bringing real-world examples to light for clients.”

A relevant audit

Firms have been using AI products for anomaly detection and analytics in audit for a few years now. Companies like MindBridge AI came on the scene and started to show the profession the real-world implications of being able to read every piece of data in minutes, as opposed to just sampling data. Samantha Bowling, a partner at Garbelman Winslow CPAs, saw the opportunity in MindBridge AI three years ago, and brought the technology to her firm.

In 2017, while Bowling served on the Governing Council for the American Institute of CPAs, she listened to president and CEO Barry Melancon describe how Big Four firm KPMG was investing millions of dollars into AI-driven audit technology.

“He was talking about how they were going to take over the world,” Bowling recalled. “As a small-firm audit partner, I was concerned, because if the big firms are doing something, sometimes it doesn’t become available to us for a while, or ever. I was actually concerned about eventually having to find a new revenue source.”

She called her existing audit software provider and asked explicitly if they had plans to embed AI into their platform. They didn’t. So Bowling did some online research and found MindBridge AI.

Bowling says that Garbelman Winslow is still in the adoption phase of MindBridge. As is true with the other technologies featured here, there is no substitute for time to allow an artificial intelligence platform to live up to its true potential. She started by engaging MindBridge for just one audit, and then grew usage from there. It helped when MindBridge integrated with QuickBooks, which made data transfers easier.

The biggest benefit of applying artificial intelligence to audit, for Bowling, is the risk analysis.

“Now that there is a direct link between QuickBooks Online and MindBridge, it automatically connects and does the risk analysis,” Bowling said. “I used to think MindBridge was an audit stamping tool that looked at transactions and identified anomalies, directing our attention and telling us where to look. But I realized it’s actually a great risk assessment tool in the very beginning of an audit.”

Bowling explained that while audits are based in risk assessment, a lot of the time, auditors have no idea where the risk is. “We only have our professional skepticism — there’s no one to tell us the risk is in revenue or payroll,” she said. “Now we have something that tells us where it is at the outset. Audit assertions are built into it.”

But there is friction in adoption. Not every client is easy to work with in MindBridge. There is still a lot of manual work to be done to transfer data that is not in the cloud, for instance, to MindBridge AI’s platform.

“Everyone just wants it to be an easy thing — to upload the general ledger and get going — but I think they’d be remiss not to do this with at least one client, or start with their cloud-based clients first before going to challenging clients,” Bowling said. “People are looking for faster, better ways, but I went into this not to do a faster audit but a relevant audit.”

Bowling received CPA.com’s Innovative Practitioner Award in 2018 for her work bringing AI to Garbelman Winslow CPAs. She won in part for the fact that it is small business and nonprofit clients to which she is bringing AI-enabled services, which also has the side benefit of Bowling being able to pass the cost of using MindBridge to her clients by folding it into the billing package. Nonprofit clients don’t mind paying top dollar for service that guarantees an accurate risk assessment.

“Nonprofit clients don’t care about us passing the fee onto them to minimize risk as much as we do, because nonprofit board members are just worried about someone doing something wrong with the money and it being in the newspaper,” Bowling said. “So they’re happy to have a very good audit done, and pay for it.”

Every transaction in the world

When thinking about the application for artificial intelligence in tax, often we think about tax preparation, since there is a lot of room to automate it. In fact, Samantha Bowling said that if she could apply AI to any other service area at her firm, it would be tax: “The current process, with a mix of paper documents and e-returns, is asinine,” she said. “I can’t wait till the whole process is 100 percent automated.”

AI-related innovation in tax prep is moving slowly, although the Internal Revenue Service has started to use the technology in different capacities to detect tax evasion and other types of noncompliance. But of course, there are other areas of tax that are ripe for disruption with AI, and sales tax automation is one.

One of the companies working in this area, Avalara, has made investments in AI in recent years, one of which was acquiring Indix in 2019. Indix was based on an idea that founder Sanjay Parthasarathy had for creating a comprehensive index of retail product information online using artificial intelligence to aggregate the data. (The aggregator was built in layers, with a Google web crawler grabbing information from all over the internet, and then various smart algorithms working together to curate and organize that data.)

Brands and retailers could buy access to this database of information on mostly retail, but also some business-to-business, products, to enrich their catalogs, benchmark against competitors, and so on. Basically, Indix was built as a neutral aggregator of e-commerce inventory.

And now, Avalara owns that AI-built index of more than 4 billion products. This means that Avalara can fold categorization data for much of the world’s online inventory of products in with its tax content database, which includes international product codes and classifications; taxability rules; exemption conditions; tax holidays; jurisdictions; boundaries; tax rates; thresholds and registration, compliance, and return preparation and filing requirements.

If this list sounds daunting, that’s kind of the point: Avalara’s mission is to “to be a part of every transaction in the world.” Without AI enabling at least some of this technology, this would be an impossible goal.

“When you buy a tax compliance product or suite, you want to be able to start using it tomorrow,” said Parthasarathy, who now serves as chief product officer for Avalara. “However, you know that before you can use an automated system, you have to make sure the tax nexus is right, the catalog is mapped to the tax code, a set of things that take time and research. If you want to start selling internationally, and you therefore need to start using harmonized tax codes — if it’s going to take nine months to do it, that’s lost value. We can get you going right away.”

Before Parthasarathy founded Indix, he spent almost two decades at Microsoft. He ended his career there in 2009 as corporate vice president of the Startup Business Accelerator program, a program he created; and he was director of Bill Gates’ 1997 trip to India, which led to a significant investment in that country by the software giant.

When talking about historical AI, Parthasarathy will sometimes use the term neural networks, which are indeed the statistical model programs ancestor to what we call AI today. His knowledge of AI is deep and historical, from having spent so many years helping build one of the most innovative companies in recent history. From his vantage point, he sees both the immense possibilities of AI, as well as the risks.

“There are risks in tax — compliance has potential penalties if done incorrectly,” he commented. “You’re doing it on behalf of somebody, so you want to make sure it is accurate and appropriate. You probably want actual people to keep an eye on it, rather than let AI run everything, even if one day it can. There is an ethical risk — when you have all this data, what is the responsibility of the government and companies to treat it as private data?”

نشر في

تكنولوجيا المعلومات

الأحد, 17 يناير 2021 13:40

توقعات الرؤساء الماليين في السوق المتوسطة لعام 2021

يتوقع غالبية الرؤساء الماليين في السوق المتوسطة حدوث انتعاش اقتصادي وزيادة الإيرادات لشركاتهم في عام 2021

معلومات إضافية

-

المحتوى بالإنجليزية

Midmarket CFOs expect revenue growth in 2021

By Michael Cohn

A majority of middle-market CFOs are predicting an economic recovery and revenue increases for their companies in 2021, according to a new survey by BDO USA.

The 2021 BDO Middle Market CFO Outlook Survey, found that 60 percent of the 600 CFOs polled at midsized companies anticipate economic recovery, while 56 percent expect revenue increases, in 2021. In addition, 62 percent of the survey respondents anticipate their company will be thriving a year from now.

Nearly three-fourths of the middle-market CFOs said their companies received government assistance as a result of the crisis. Cost cutting and reorganization for resilience are the top priorities for many CFOs.

The pandemic made an impact on nearly every company, and 39 percent of the CFOs polled indicate that the pandemic accelerated digital transformation at their companies, while 38 percent said it opened new expansion opportunities for products or services and 31 percent for new geographies.

“Unprecedented was the buzzword in 2020 for good reason,” said BDO USA CEO Wayne Berson in a statement. “Many middle-market companies persevered through levels of transformation and disruption in one year akin to what some companies experience in a full lifecycle. But rather than hunker down and endure, middle market leaders endeavor to move forward to refresh strategy and enhance agility. While we’re not out of the woods, the middle market is poised to pivot to new levels of potential.”

Deal flow was unsteady last year as CFOs assessed and reassessed the possible outcomes of the pandemic’s impact on their business. However, CFOs appear to be more optimistic this year, with 29 percent planning to seek private equity investment, 24 percent want a merger or acquisition and 20 percent hope to pursue an IPO.

While returning to the office or floor is critical for many CFOs, 43 percent of the respondents said they would increase or establish permanent remote work options. Office space is likely to be downsized, with 28 percent of the CFOs polled planning to eliminate or consolidate their current real estate footprint. CFOs also intend to build a more flexible workforce through automation (38 percent) and outsourcing (32 percent).

The main threats cited by the CFOs include a prolonged economic downturn, competitive pressure, supply chain disruption and falling behind on technology or innovation.

Coming out of an election year, tax challenges are also going to be important, with understanding total tax liability (19 percent) and navigating shifting trade and tariff policies (17 percent) among the top challenges cited by the CFOs. Managing disclosures and risk factors is also a top financial reporting challenge as the CFOs try to assess how to communicate impact of COVID-19 on matters that may be material to stakeholders.

نشر في

موضوعات متنوعة

موسومة تحت